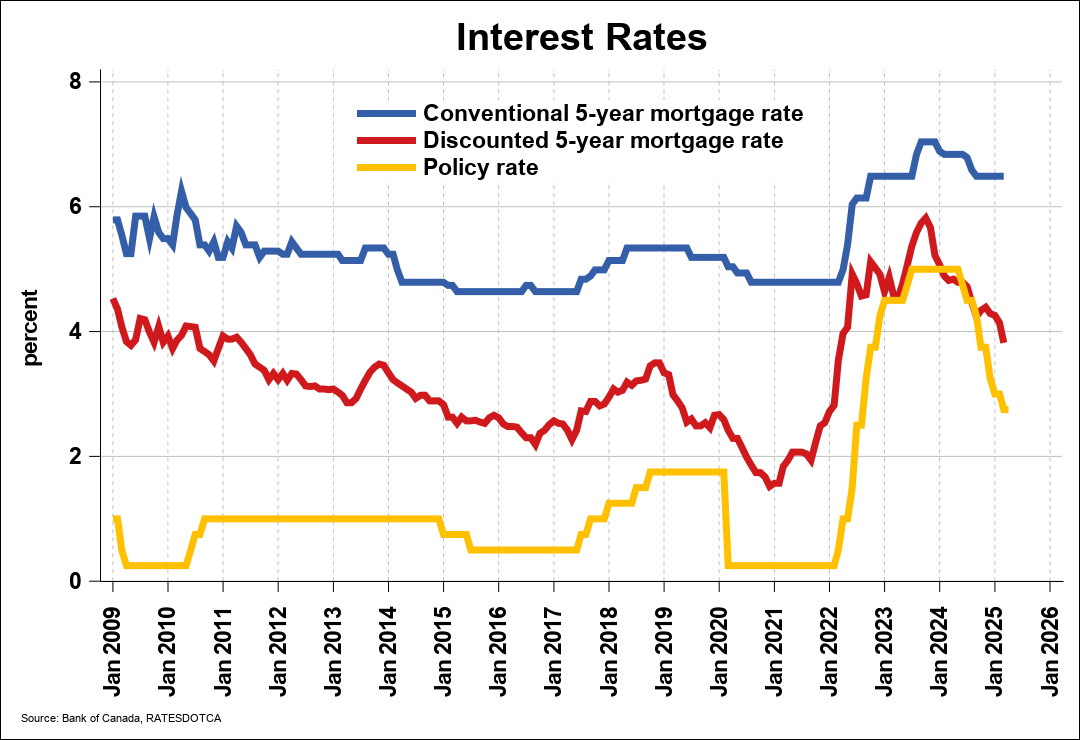

Bank of Canada Maintains Rate at 2.75%

On Wednesday, June 4, 2025, the Bank of Canada held its target for the overnight lending rate at 2.75%, marking the second consecutive decision to hold rates steady, following a series of cuts that began in April 2024.

The Bank emphasized that uncertainty surrounding U.S. trade policy remains elevated, with the current U.S. administration continuing to increase and decrease various tariffs, including the recent doubling of tariffs to 50% on steel and aluminum, along with new trade actions still being threatened.

The Bank observed that Canada’s first quarter Gross Domestic Product (GDP) growth came in at 2.2% which was slightly above the Bank’s forecast. Growth was primarily driven by a pull-forward in exports and building inventory in anticipation of tariffs.

The Bank also noted that consumer confidence was down, with the housing market showing signs of slowing, driven by a sharp contraction in resales. The labour market has weakened, particularly in trade-sensitive sectors, with unemployment rising to 6.9%.

The Bank expects the economy to be considerably weaker in the second quarter, with the strength in exports and inventories reversing and final domestic demand remaining subdued.

Consumer Price Index (CPI) inflation eased to 1.7% in April, largely due to the removal of the federal consumer carbon tax. However, excluding the consumer carbon tax, inflation rose slightly to 2.3%, which was above expectations. Recent surveys conducted by the Bank indicate that households and businesses both expect tariffs to raise prices, with many companies planning to pass on higher costs to consumers, meaning more inflation to come.

Given the mixed signals in the economy, the Governing Council opted to hold rates steady as they gain more information on U.S. trade policy and its impacts on the Canadian and global economy. In its closing notes, the Bank stated that its focus would remain on price stability for Canadians, paying particular attention to the following risks and uncertainties:

the extent to which higher tariffs reduce demand for Canadian exports;

how much this spills over into business investment, employment and household spending;

how much and how quickly cost increases are passed on to consumer prices; and

how inflation expectations evolve.

One could also add to that upcoming COVID-era mortgage renewals, and the impact of so much discretionary income being diverted toward mortgage interest payments on the economy in the coming years.

The Bank reaffirmed its commitment to price stability through this period of global upheaval, noting it will proceed cautiously to support economic growth while ensuring inflation remains well controlled.

The Bank of Canada will make its next scheduled interest rate announcement on July 30, 2025, and will publish its updated outlook for the economy and inflation in its Monetary Policy Report at that time.